There’s no doubt that pricing plays an important role in a customer’s decision making process. Yet many SMME business owners have difficulty or challenged by understanding the best prices to charge for their goods or services. This is especially true if you’re a new business owner tasked with pricing your products or services for the first time in a competitive market.

The prices set for goods or services influence nearly every aspect of our business, including things like cash flow, profit margins, operating expenses, and the perception of the value of our products/services in the market. So, choosing them wisely is critical for business scalability and staying competitive in your niche.

Thankfully, there are tried-and-tested pricing methods that several businesses can turn to.

Value-Based Pricing

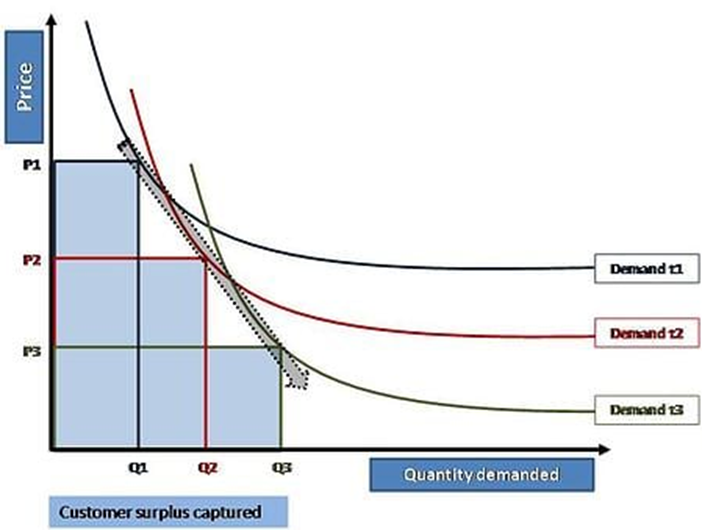

Value-based pricing is a pricing strategy used by businesses to charge products and services at a rate they believe consumers are willing to pay. As opposed to calculating production costs and applying a standard markup, businesses instead gauge the perceived value to the customer and charge accordingly

Artwork, cars, amusement parks, and even social media influencers use value-based pricing to sell their products and services. All three of these industries take into account a few standard truths about value-based pricing:

- The market influences how much a consumer will be willing to pay for a product.

- The benefit that the product provides to the customer influences the value of that product.

- Competitors’ pricing can influence how valuable consumers perceive a product to be.

Competitive Pricing Strategy

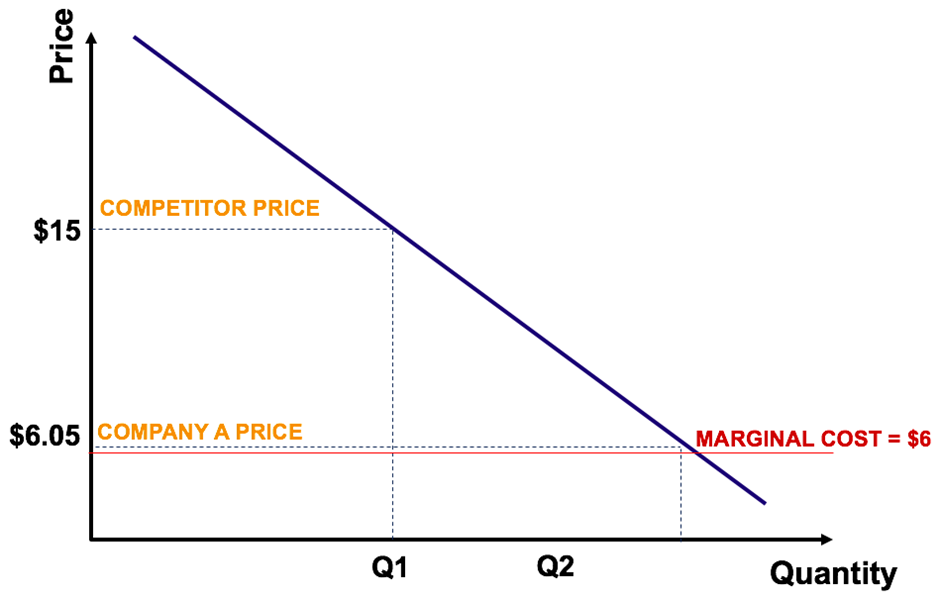

Competitive pricing is the process of strategically selecting price points for your goods or services based on competitor pricing in your market or niche, rather than basing prices solely on business costs or target profit margins. Competitive pricing is typically used by businesses that sell the same or highly similar products in the same market for an extended period, as prices of these products often reach a level of equilibrium.

Using a pricing strategy based on competition, businesses have three choices when establishing prices for their goods or services:

- Lower Prices: The prices of your goods or services are lower than your competitors’ prices in your market. This strategy can be lucrative for businesses that are able to capitalize on economies of scale. Lower price points can also be used as part of a loss leader strategy. Frequently implemented by businesses entering a market for the first time, a loss leader strategy is a technique in which goods or services are set at a lower price point that’s not profitable but draws in new customers or enables a business to sell additional, more profitable goods or services to those customers.

- Higher Prices: The prices of your goods or services are higher than your competitors’ prices in your market. This strategy is used by businesses that offer goods or services with more features or benefits than their competitors. Higher price points are typically used by businesses that have a well-established brand reputation and provide a “premium” or “luxury” product compared to other businesses in their market or niche.

- Price Skimming: When businesses introduce a new product into the market, they can use price skimming as a competitive pricing strategy. Price skimming is the technique of charging the highest initial price that customers will pay when demand is high, and then lowering that price over time. Once as much revenue is made as possible and competition starts to enter the market, businesses can lower their product prices to attract new cost-conscious customers while staying competitive against competitors who are now producing similar products.

- Equal Prices: The prices of your goods or services are equal to your competitors’ prices in your market, or to the prevailing market price. Businesses that select equal price points to their competitors typically try to differentiate themselves by doing things like creating unique shopping experiences or offering more attractive product alternatives (e.g., using sustainable materials or manufacturing processes to attract eco-conscious audiences, etc.).

- Price Matching: When businesses are unable to collect, analyze, and act on competitor pricing data or fluctuations in a timely manner, price matching is another competitive pricing strategy. Businesses that offer price matching options for their customers can stay competitive in their market without having to closely follow their competitors’ pricing strategies, or constantly update their point of sale (POS) system or eCommerce store.

Price Skimming Strategy

Price skimming is a pricing strategy where the price of goods or services is set high at the time of launch and then lowered as consumers become more familiar with it. This method targets early adopters and does not target the mass market.

A variant of this strategy is called penetration pricing, which sets high launch prices to penetrate markets.

Customers known as early adopters will pay steeper prices for a cutting-edge product if it’s marketed as a “must-have”, whether the price accurately reflects the value or not. Eventually, prices are lowered to follow the product demand curve and attract more price-sensitive customers.

Cost-plus pricing

Cost-plus pricing is also known as markup pricing. It’s a pricing method where a fixed percentage is added on top of the cost it takes to produce one unit of a product. The resulting number is the selling price of the product.

This pricing method looks solely at the unit cost and ignores the prices set by competitors. For this reason, it’s not always the best fit for many businesses because it doesn’t take external factors, like competitors, into account.

Retail companies like clothing, grocery, and department stores often use cost-plus pricing. In these cases, there is variation in the items being sold, and different markup percentages can be applied to each product.

If you sell software as a service (SaaS), this pricing method isn’t the best fit because the value your products provide is often more significant than the costs to produce the products.

The cost-plus pricing method is a good fit for businesses that want to pursue a cost-leadership strategy. Cost-plus pricing can be used as part of the company’s value proposition by sharing its pricing policy with consumers and saying something like, “We’ll never charge more than X% for our products.” This transparency helps build trust with potential customers and allows businesses to build a reputable brand.

Penetration Pricing

Penetration pricing is a pricing strategy that is used to quickly gain market share by setting an initially low price to entice customers to purchase. This pricing strategy is generally used by new entrants into a market. An extreme form of penetration pricing is called predatory pricing.

It is common for a new entrant to use a penetration pricing strategy to quickly obtain a substantial amount of market share. Price is one of the easiest ways to differentiate new entrants from existing market players. The overarching goal of this pricing strategy is to:

- Capture market share

- Create brand loyalty

- Switch customers from competitors

- Generate significant demand, looking to utilize economies of scale

- Drive competitors out of the market

– When there is little product differentiation

– Demand is price-elastic

– Where the product is suitable for a mass market (and, therefore, for utilizing economies of scale)

Economy Pricing Strategy

Economy pricing allows businesses to price products according to their production value because they don’t acquire the extra costs of advertising or marketing.

But making a profit with economy pricing is a volume game — meaning the only way to a profit is to consistently entice a large number of customers.

Production costs, profit margins, and cost are the three factors behind economic pricing. Use the following equation to calculate prices:

PRICE = PRODUCTION COST + PROFIT MARGIN

Production cost is the amount of money that goes into creating a product. It includes a variety of expenses, from labor to raw materials. Profit margin indicates the profitability of a product or service. Businesses should consider both these factors to determine how low they can make their prices.

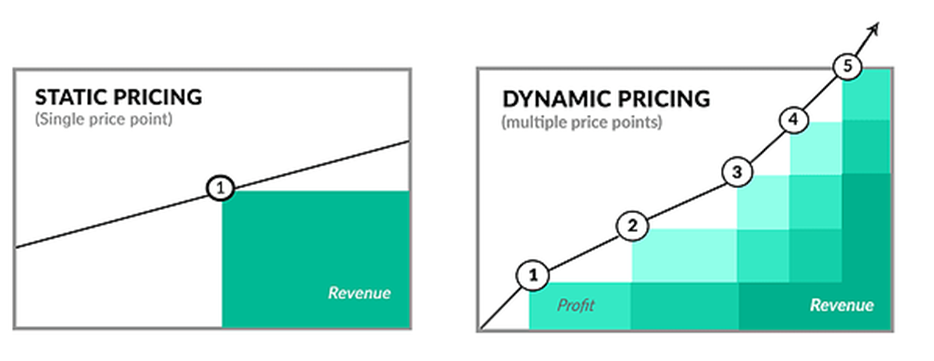

Dynamic Pricing

Dynamic pricing — also known as surge pricing, demand pricing, or time-based pricing — is a strategy where businesses adjust the prices of their offerings to account for changing demand. For instance, an airline will shift seat prices based on seat type, number of remaining seats, and time until the flight.

Opposed to static pricing, dynamic pricing helps your business maximize profit by operating at multiple price points.

However, this strategy isn’t for everyone. For instance, restaurants use static pricing, regardless of how many customers are seated. Many manufacturers do the same.

To determine if the dynamic pricing model suits your business, consider these questions.

- Can your business gauge how and when demand shifts? If your company has no reference points for understanding how its market fluctuates, it won’t be able to effectively adjust prices to suit changing demand.

- Will your customers be okay with non-static prices? Your company can’t successfully use dynamic pricing if potential consumers are reluctant to pay extra. This strategy is even more difficult if your industry has established pricing structures. Your consumers could churn if you increase your prices while your competitors don’t.

- Is your company a market leader? An organization can only set prices at will if it has a significant place in its market. If a relatively small business in a crowded industry raises prices on a whim, customers could easily switch to a competitor.

- Do your industry peers use dynamic pricing? Using dynamic pricing is an excellent idea if it’s common in your industry. This makes sense because your competitors have already validated that dynamic pricing works